The UK Patent Box regime was updated in 2016 with a five-year transitional period for those companies that had already entered the scheme prior to the new changes. Nearly a year on from the end of this transitional period, we look at the impact of these updates to the regime and what the 2021 statistics produced by HMRC suggest about the usage of the scheme.

What is the UK Patent Box?

The UK Patent Box scheme was introduced in April 2013 and allows UK companies to elect to pay a reduced rate of corporation tax on profits derived from the exploitation of patents and certain other types of Intellectual Property such as Supplementary Protection Certificates (SPCs) for pharmaceutical products.

In order to benefit from the scheme, a company must satisfy three basic criteria:

- It must have a qualifying IP right. Qualifying IP rights are:

- Patents granted by the UKIPO or the EPO;

- Patents granted by some, but not all, states in the European Economic Area (EEA); and

- Certain other European IP rights (e.g. SPCs, plant breeders’ rights, plant variety rights).

- It must “actively hold” the qualifying IP right as an owner or an exclusive licensee. The company must be creating, or significantly contributing to, the protected invention, or performing a significant amount of activity to develop the protected invention or any product or process incorporating the protected invention. If a company is part of a group and satisfies this requirement through the activities of another group member, the company in question must actively manage its portfolio of qualifying IP rights; and

- It must have an income related to the qualifying IP right (e.g. sales of patented products).

In effect, the Patent Box allows for a 10% corporate tax rate, rather than the current rate of 19%, on qualifying profits derived from UK or European patents.

2016 changes

In May 2016, we reported changes that were to be made to the UK Patent Box in response to an October 2015 report in which the Organisation for Economic Co-operation and Development (OECD) identified the UK Patent Box as being a ‘harmful tax practice’. The UK government announced a consultation and, in December 2015, draft legislation was published.

The reason for the change in the scheme was that the original legislation did not require a claimant for tax relief to carry out any Research & Development (R&D) in the UK. Following the introduction of the Patent Box in April 2013, a number of multinational companies sought to take advantage of the regime by relocating their tax domicile to the UK, prompting some EU states, most notably Germany, to claim that the UK Patent Box scheme could provide scope for abusive tax avoidance practices.

The updated UK Patent Box regime, which has been in force since 1st July 2016, introduced a “modified nexus approach” by which the amount of tax relief available will depend on the extent to which the R&D leading to the patented invention (or a product embodying it) was carried out in the UK. Some of the R&D may be outsourced or acquired, but only to a cap of 30% of the qualifying expenditure. The hope was that this would allow the UK Patent Box to fulfil its intended purpose, namely incentivising innovative companies to develop new patented products in the UK, more successfully, whilst minimising the opportunity for tax avoidance.

A transitional period was provided that enabled companies that had already entered the scheme before this date (i.e. by 30th June 2016) to benefit from the old rules. This transitional period ended on 30th June 2021, meaning that all participants from 1st July 2021 onwards are now subject to the updated rules.

How has the scheme progressed?

When we reported the changes that were to come into force in July 2016, we noted criticism from some observers that the updated rules would considerably increase the administrative cost of compliance on companies wishing to take advantage of the scheme, and that small and medium-sized enterprises (SMEs) with limited resources could be penalised. In March 2019, we reported on initial statistics published in September 2018 by HM Revenue & Customs (HMRC) suggesting that this might indeed have been the case.

Subsequently, in March 2021, we reported on updated HMRC statistics published in September 2020. The findings in that report can be summarised as follows:

- Like the September 2018 report, the September 2020 report confirmed that both the number of companies claiming Patent Box relief and the total value of relief claimed continue to grow year on year.

- Large companies accounted for 28% of the companies claiming relief in 2017-2018, which was very much in line with figures reported in previous years, but only accounted for 92% of the total relief claimed. Whilst this second figure was still a significant proportion, it did represent a meaningful decrease from 95.5% in 2015-2016 and 96.3% in 2017-2018, which suggested to us that small and, particularly, medium-sized companies may have been getting to grips with the stricter rules introduced in 2016.

- Companies in London represented the highest proportion of relief claimed, which mirrored previous years.

- The industry sector representing the highest proportion of relief claimed was Finance and Insurance, despite only ten companies in this sector claiming relief.

September 2021 statistics

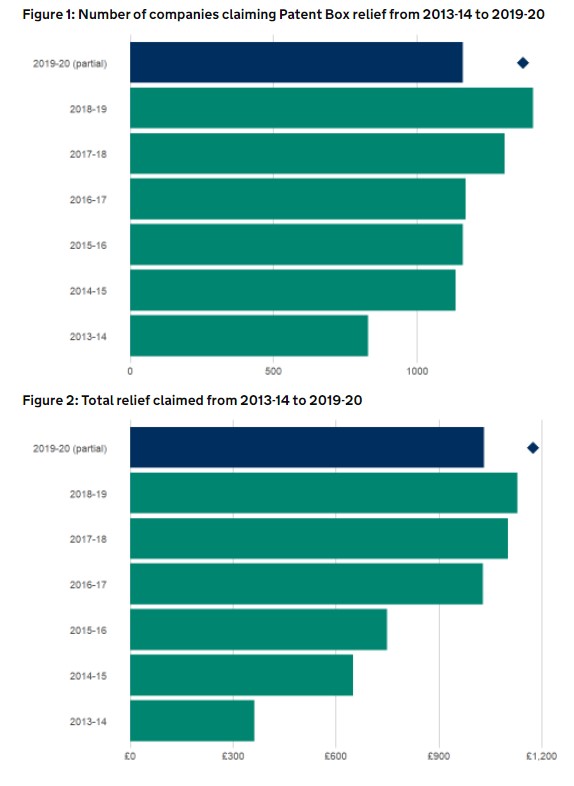

Further updated statistics were published by HMRC in September 2021. The September 2021 statistics provide complete data for the tax year covering the period 1st April 2018 to 31st March 2019, as well as projected statistics for the tax year 2019 to 2020.

As in previous years, the September 2021 statistics show that London-based companies claimed by far the largest proportion of relief in the tax year 2018 to 2019 (48%). It is projected that this could increase to 50% in 2019 to 2020, emphasising the gap between London and the rest of the UK.

The September 2021 report gives an overview of i) the number of companies claiming relief through the Patent Box and ii) the total relief claimed. These statistics are shown relative to previous years in Figures 1 and 2 below (total relief numbers in Figure 2 are given in thousands). The numbers for 2019 to 2020 include the partial value for data collected so far, as well as a projected value (shown as a diamond).

The statistics show that both the number of companies claiming relief and the total relief claimed continued to grow year on year through 2018 to 2019. Interestingly, the projected figures for 2019 to 2020 suggest that, whilst it is expected that the total relief claimed will continue to grow, the number of companies claiming relief may fall slightly. This adds weight to observations that we made when the 2016 changes were first introduced that large and mid-size companies may find the more stringent requirements associated with the newer regime easier to comply with than smaller companies and young start-ups.

A helpful way to supplement this analysis is to look at the proportion of overall relief that is claimed by large companies. The September 2020 statistics indicated that large companies were responsible for 92% of the overall relief claimed in the tax year 2017 to 2018, and the September 2021 statistics confirm that this number remains the same for 2018 to 2019.

This, paired with the partial 2019 to 2020 information provided in Figures 1 and 2 indicating that the overall relief is expected to increase whilst the number of companies claiming relief may decrease, could indicate that a significant number of mid-size companies are taking advantage of the scheme.

The sector analysis in the September 2021 statistics also lends weight to this proposition. We reported in March 2021 that the industry sector representing the highest proportion of relief claimed in the tax year 2017 to 2018 was Finance and Insurance, despite only ten companies in this sector claiming relief, suggesting that very large companies were contributing significantly to the overall relief claimed. The September 2021 statistics show that in the following year, 2018 to 2019, 32% of the total relief claimed was by groups in the Manufacturing sector and 26% was by groups in the Professional, Scientific and Technical sector (an area in which one would expect meaningful research and development to take place). HMRC projects that these two sectors combined will continue to make up a majority of both the number of groups claiming and the total relief in the year 2019 to 2020, again perhaps hinting at a trend in mid-size companies using the scheme to good effect.

We will continue to monitor the development of the UK Patent Box with interest.